Buy to Let

Investing in Buy-to-Let properties can be a lucrative venture, offering potential for long-term capital growth and a steady rental income stream.

Here's why it's worth considering BTL investments, along with details on the products available, affordability assessment, and deposit requirements:

-

Why Invest in Buy-to-Let Properties

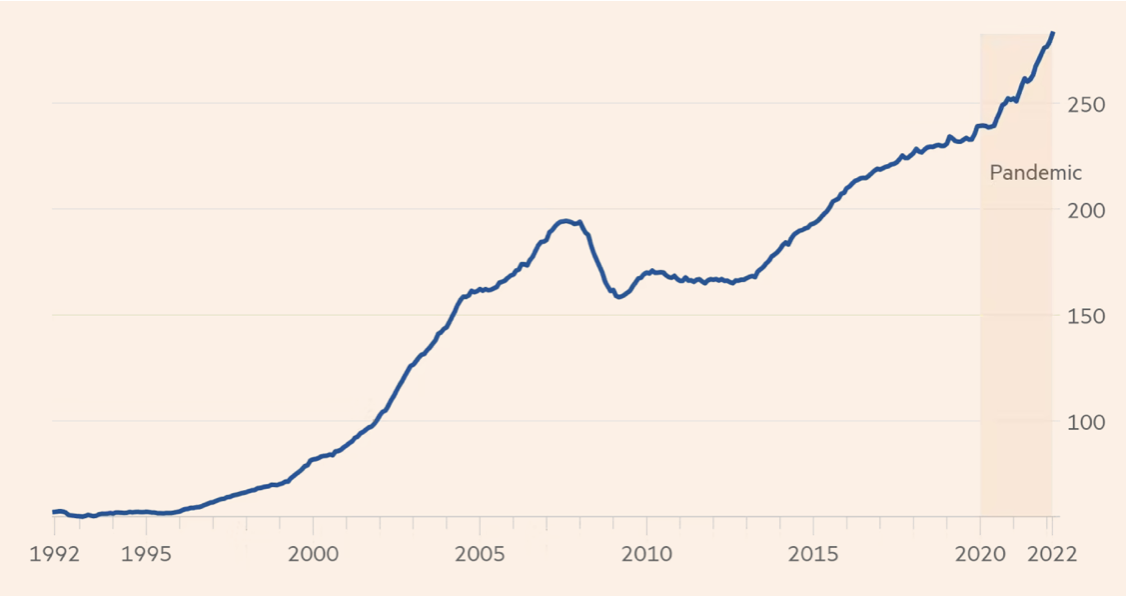

BTL properties can provide a stable source of income through rental payments, potentially offering higher returns compared to other investment options. Property investment often serves as a hedge against inflation, with property values historically appreciating over time. The graph below shows the average house prices since 1992.

SOURCE FINANCIAL TIMES

https://www.ft.com/content/db2adf81-6a22-49ef-9294-9bdf27c7c71d

Diversifying your investment portfolio with BTL properties can spread risk and provide a tangible asset that can be leveraged for further investment opportunities. With the growing demand for rental accommodation, particularly in urban areas and university towns, BTL properties offer the potential for consistent demand and occupancy rates.

Types of BTL Mortgage Products:

- Fixed-Rate Mortgages:

Provide the security of a fixed interest rate for a predetermined period, offering stability in mortgage payments.

Tracker Mortgages: Linked to an external interest rate, such as the Bank of England base rate, with mortgage payments fluctuating in line with changes in the interest rate.

Interest-Only Mortgages: Require borrowers to only repay the interest on the loan during the mortgage term, with the capital amount repaid at the end of the term. This is the most popular type of product chosen by landlords. - Specialist BTL Products:

Tailored to specific investor profiles, such as first-time landlords, Limited Company Special Purpose Vehicle (LTD SPV) Mortgages, portfolio landlords, or those investing in Houses in Multiple Occupation (HMOs) or multi-unit properties. - Affordability Assessment and Stress Testing:

Lenders typically assess affordability for BTL mortgages based on the property's rental income, requiring a minimum rental yield to cover mortgage payments. The stress test for affordability involves assessing whether the rental income is sufficient to cover mortgage payments even in scenarios of potential interest rate rises or rental void periods. Lenders may apply a Rental Coverage Ratio (RCR), requiring the rental income to exceed a certain percentage of the mortgage payments, typically around 125% to 145%.

The ICR formula to calculate the minimum rental income required is loan amount x interest stress rate x taxpayer stress rate / 12 = the monthly minimum. The ICR to calculate the maximum loan amount is monthly rental income x 12/ interest stress rate / taxpayer stress rate = maximum loan amount.

Example

ICR formula to calculate minimum rental income required.

Loan Amount: £200,000

Interest stress rate: 5.5%

Taxpayers stress rate: 125%

((£200,000 x 5.5%) x 125%)/12 = £1,146*

The ICR to calculate the maximum loan amount is:

((£1,146*x12)/5.5%)/125%= £200,000

*Rounded up to the nearest whole number

-

Deposit Requirements

BTL mortgages generally require a higher deposit compared to residential mortgages, with typical deposit amounts ranging from 20% to 25% of the property's purchase price. Higher deposits may be required for more favourable mortgage rates or to meet lender criteria, particularly for investment properties with higher perceived risk. Investing in Buy-to-Let properties offers the potential for significant financial rewards, but it's essential to carefully consider the associated risks and costs. Our experienced mortgage advisors can provide personalised guidance and help you navigate the complexities of BTL investments, from product selection to affordability assessment and securing the right financing solution for your investment goals. Contact us today to explore your options and start building your property investment portfolio with confidence. -

BTL Remortgage

BTL remortgage allows existing landlords to switch to a new mortgage deal, potentially securing better terms, rates, or releasing equity from their property portfolio. Our team can assist you in exploring BTL remortgage options, ensuring you make informed decisions to optimise your property investment strategy. Please check out our dedicated section where you can find more information about remortgaging. (add a hyperlink to remortgage section from residential).

When exploring investment opportunities in the property market, understanding the difference between Standard Buy-to-Let (BTL) and Special Purpose Vehicle (SPV) Buy-to-Let mortgages is crucial for investors. These financing options cater to different investor profiles and offer distinct advantages and limitations. This section aims to clarify these differences, assisting our clients in making informed decisions.

Definition and Structure

Standard Buy-to-Let Mortgages are traditional loan arrangements offered to individual investors or partnerships looking to purchase property to rent out. These mortgages are assessed based on the individual’s income, credit history, and the potential rental income of the property. SPV Buy-to-Let Mortgages are designed for properties bought through a Special Purpose Vehicle, a type of limited company formed specifically for owning and managing properties. An SPV operates under specific SIC codes related to real estate, making it easier for lenders to understand the business purpose.

How to they differ?

- Tax Considerations

A significant difference lies in tax treatment. Individual investors with Standard BTL mortgages are taxed on rental income as personal income, which could push them into higher tax brackets. In contrast, an SPV BTL structure allows investors to be taxed under corporate tax rates, which can be more favourable. Additionally, mortgage interest can be fully deducted as a business expense in an SPV, offering further tax efficiency. - Legal and Financial Separation

An SPV provides a legal and financial separation from the investor’s personal finances. This structure limits personal liability, as the SPV owns the property and any debts or liabilities are contained within the company. For individual BTL mortgages, investors are personally liable, affecting their credit rating and risk exposure. - Setup and Operational Complexity

Setting up and managing an SPV involves additional complexity and costs, including company formation, accounting, and compliance with corporate governance. For individual investors not prepared to handle these aspects, a Standard BTL mortgage offers a simpler route to property investment. - Flexibility and Portfolio Expansion

Finally, flexibility and portfolio expansion differ significantly. SPV BTL mortgages are advantageous for investors looking to build a large property portfolio efficiently under one corporate umbrella, simplifying management and scaling. Standard BTL mortgages are more suited to investors with a smaller number of properties, offering less complexity in management but also less scalability.

Conclusion

Both Standard BTL and SPV BTL mortgages have their place in property investment. The choice between them depends on the investor's financial situation, tax considerations, risk appetite, and long-term investment strategy. Polish brokers play a vital role in guiding investors through these options, ensuring they align with their investment goals and financial planning.